DRS/A: Draft registration statement submitted by Emerging Growth Company under Securities Act Section 6(e) or by Foreign Private Issuer under Division of Corporation Finance policy

Published on February 7, 2024

Table of Contents

CONFIDENTIAL TREATMENT REQUESTED BY VIKING HOLDINGS LTD

PURSUANT TO 17 CFR 200.83.

As submitted confidentially with the U.S. Securities and Exchange Commission on February 7, 2024. This Amendment No. 1 to the draft registration statement has not been publicly filed with the U.S. Securities and Exchange Commission and all information herein remains strictly confidential.

Registration No. 333-

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM F-1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

Viking Holdings Ltd

(Exact name of Registrant as specified in its charter)

Not Applicable

(Translation of Registrants name into English)

| Bermuda | 4400 | Not Applicable | ||

| (State or other jurisdiction of incorporation or organization) |

(Primary Standard Industrial Classification Code Number) |

(I.R.S. Employer Identification Number) |

94 Pitts Bay Road

Pembroke, Bermuda HM 08

Tel: (441) 478-2244

(Address, including zip code, and telephone number, including area code, of Registrants principal executive offices)

Leah Talactac

Chief Financial Officer

5700 Canoga Avenue

Woodland Hills, CA 91367

Tel: (818) 227-1234

(Name, address, including zip code, and telephone number, including area code, of agent for service)

Copies to:

| Gregg A. Noel Ryan J. Dzierniejko Skadden, Arps, Slate, Meagher & Flom LLP 525 University Ave. Palo Alto, CA 94301 Tel: (650) 470-4500 |

Christopher D. Lueking Scott W. Westhoff Jonathan E. Sarna Latham & Watkins LLP 330 N. Wabash Avenue, Suite 2800 Chicago, IL 60611 Tel: (312) 876-7700 |

Approximate date of commencement of proposed sale to the public: As soon as practicable after the effective date of this Registration Statement.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check the following box. ☐

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

Indicate by check mark whether the registrant is an emerging growth company as defined in Rule 405 of the Securities Act of 1933. Emerging growth company ☐

If an emerging growth company that prepares its financial statements in accordance with U.S. GAAP, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 7(a)(2)(B) of the Securities Act. ☐

The registrant hereby amends this registration statement on such date or dates as may be necessary to delay its effective date until the registrant shall file a further amendment which specifically states that this registration statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933, as amended, or until the registration statement shall become effective on such date as the Securities and Exchange Commission, acting pursuant to said Section 8(a), may determine.

Table of Contents

CONFIDENTIAL TREATMENT REQUESTED BY VIKING HOLDINGS LTD

PURSUANT TO 17 CFR 200.83.

The information in this preliminary prospectus is not complete and may be changed. We may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This preliminary prospectus is not an offer to sell, and it is not soliciting an offer to buy, these securities in any jurisdiction where the offer or sale is not permitted.

Subject to completion, dated , 2024

PRELIMINARY PROSPECTUS

Viking Holdings Ltd

Ordinary Shares

This is an initial public offering of the ordinary shares of Viking Holdings Ltd. We are offering ordinary shares. Prior to this offering, there has been no public market for our ordinary shares. We anticipate that the initial public offering price will be between $ and $ per ordinary share. We intend to apply to list our ordinary shares on the New York Stock Exchange (NYSE) under the symbol VIK.

We have two classes of shares: ordinary shares and special shares. The rights of the holders of our ordinary shares and our special shares are identical, except with respect to voting. Each ordinary share is entitled to one vote per share. Each special share is entitled to 10 votes per share. See Description of Share Capital. As a result of its ownership of special shares, our principal shareholder (as defined herein) will hold approximately % of the voting power of our issued and outstanding share capital following the consummation of this offering. As a result of our principal shareholders ownership, we will be a controlled company within the meaning of the rules of the NYSE, and we intend to rely on certain of the controlled company exemptions under the NYSE corporate governance rules.

Investing in our ordinary shares involves risks. See Risk Factors on page 29.

We are a foreign private issuer under applicable Securities and Exchange Commission rules and will be eligible for reduced public company disclosure requirements. See Prospectus SummaryImplications of Being a Foreign Private Issuer.

| Price to Public |

Underwriting Discounts and Commissions(1) |

Proceeds, Before Expenses, to Us |

||||||||||

| Per Ordinary Share |

$ | $ | $ | |||||||||

| Total |

$ | $ | $ | |||||||||

| (1) | We have agreed to reimburse the underwriters for certain expenses in connection with this offering. See Underwriting for additional information regarding underwriting compensation. |

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

We have granted to the underwriters a 30-day option to purchase up to additional ordinary shares from us at the initial public offering price less the underwriting discounts and commissions.

The underwriters expect to deliver the ordinary shares on or about , 2024.

(in alphabetical order)

| BofA Securities | J.P. Morgan | UBS Investment Bank | Wells Fargo Securities | |||

The date of this prospectus is , 2024.

Table of Contents

CONFIDENTIAL TREATMENT REQUESTED BY VIKING HOLDINGS LTD

PURSUANT TO 17 CFR 200.83.

| 1 | ||||

| 29 | ||||

| 63 | ||||

| 65 | ||||

| 66 | ||||

| 67 | ||||

| 69 | ||||

| MANAGEMENTS DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS |

71 | |||

| 93 | ||||

| 95 | ||||

| 121 | ||||

| 129 |

| 131 | ||||

| 134 | ||||

| 146 | ||||

| 148 | ||||

| 151 | ||||

| 158 | ||||

| 159 | ||||

| 159 | ||||

| 160 | ||||

| 161 | ||||

| F-1 |

Neither we nor the underwriters have authorized anyone to provide you with any information or make any representation other than the information contained in this prospectus, any amendment or supplement to this prospectus or in any free writing prospectus we may authorize to be delivered or made available to you. We take no responsibility for, and can provide no assurance as to the reliability of, any information other than the information in this prospectus or in any free writing prospectus we may authorize to be delivered or made available to you. The information contained in this prospectus is accurate only as of the date on the front of this prospectus, regardless of the time of delivery of this prospectus or any sale of ordinary shares. Our business, financial condition and results of operations may have changed since the date on the cover page of this prospectus. This prospectus is not an offer to sell or the solicitation of an offer to buy these ordinary shares in any circumstances under which such offer or solicitation is unlawful.

Through and including , 2024 (the 25th day after the date of this prospectus), all dealers effecting transactions in these securities, whether or not participating in this offering, may be required to deliver a prospectus. This is in addition to a dealers obligation to deliver a prospectus when acting as an underwriter and with respect to an unsold allotment or subscription.

For investors outside the United States: Neither we nor the underwriters have done anything that would permit this offering or possession or distribution of this prospectus in any jurisdiction where action for that purpose is required, other than in the United States. Persons outside of the United States who come into possession of this prospectus must inform themselves about, and observe any restrictions relating to, this offering and the distribution of this prospectus outside of the United States.

i

Table of Contents

CONFIDENTIAL TREATMENT REQUESTED BY VIKING HOLDINGS LTD

PURSUANT TO 17 CFR 200.83.

ABOUT THIS PROSPECTUS

As used in this prospectus, unless the context otherwise requires, references to we, us, our, our business, the Company, Viking and similar references refer to Viking Holdings Ltd and, where appropriate, its consolidated subsidiaries.

PRESENTATION OF FINANCIAL INFORMATION AND CERTAIN DEFINITIONS

Presentation of Financial Information

Our audited consolidated financial statements as of December 31, 2021 and 2022 and for the years ended December 31, 2021 and 2022 included in this prospectus have been prepared in accordance with International Financial Reporting Standards (IFRS), as issued by the International Accounting Standards Board (IASB). The summary consolidated financial information as of December 31, 2019 and 2020 and for the years ended December 31, 2019 and 2020 has been derived from our consolidated financial statements that are not included in this prospectus. The unaudited interim condensed consolidated financial statements as of September 30, 2023 and for the nine months ended September 30, 2022 and 2023 included in this prospectus are unaudited, and all information contained in this prospectus with respect to such periods is also unaudited.

We have made rounding adjustments to reach some of the figures included in this prospectus. As a result, numerical figures shown as totals in some tables may not be arithmetic aggregations of the figures that precede them.

In this prospectus, unless otherwise indicated, all references to U.S. dollars, dollars or $ are to the lawful currency of the United States of America and all references to euro or are to the lawful currency of the participating Member States in the Third Stage of European Economic and Monetary Union of the Treaty Establishing the European Community, as amended from time to time.

Presentation of Other Data and Certain Definitions

Unless otherwise specified or the context requires otherwise in this prospectus, all references to:

| | Adjusted EBITDA are to EBITDA (consolidated net income (loss) adjusted for interest income, interest expense, income tax expense and depreciation, amortization and impairment) as further adjusted for non-cash Private Placement derivatives gains and losses, loss on Private Placement refinancing, currency gains or losses, stock-based compensation expense and other financial income (loss) (which include forward gains and losses, gain or loss on disposition of assets, certain non-cash fair value adjustments, restructuring charges and non-recurring items); |

| | Adjusted EBITDA Margin are to the ratio, expressed as a percentage, of Adjusted EBITDA divided by Adjusted Gross Margin; |

| | Adjusted FCF Conversion are to the ratio, expressed as a percentage, of Adjusted FCF divided by Adjusted EBITDA; |

| | Adjusted Free Cash Flow or Adjusted FCF are to net cash flow from (used in) operating activities as adjusted for interest paid, interest payments for lease liabilities, interest received, and Ongoing Capex, as further adjusted for interest expense related to our Series C Preference Shares. Our Series C Preference Shares will automatically convert into ordinary shares immediately prior to the consummation of this offering; |

| | Adjusted Gross Margin are to gross margin adjusted for vessel operating expenses and ship depreciation and impairment. Gross margin is calculated pursuant to IFRS as total revenue less total cruise operating expenses and ship depreciation and impairment; |

ii

Table of Contents

CONFIDENTIAL TREATMENT REQUESTED BY VIKING HOLDINGS LTD

PURSUANT TO 17 CFR 200.83.

| | Advance Bookings are to the aggregate ticketed amount for guest bookings for our voyages at a specific point in time, and include bookings for cruises, land extensions and air; |

| | average age are, for ships or vessels, to average age of those ships or vessels weighted by berth; |

| | berth are to a space for one passenger. Almost all of our staterooms are double occupancy, or two berth staterooms, but we have some staterooms that are single occupancy, or single berth staterooms; |

| | CAGR are to compound annual growth rate; |

| | Capacity Passenger Cruise Days or Capacity PCDs, with respect to any given period, are to measurements of capacity that represent, for each ship operating during the relevant period, the number of berths multiplied by the number of Ship Operating Days, determined on an aggregated basis for all ships in operation during the relevant period; |

| | China JV Investment are to the joint venture between us and China Merchants Shekou, a subsidiary of China Merchants Group, to build a cruise line offering Chinese coastal sailing for Mandarin-speaking populations in China. The China JV Investment is comprised of two primary entities: CMV and SCM. We have a 10% interest in CMV. We have a 50% interest in SCM; |

| | China Outbound are to our outbound river cruise product marketed to Mandarin-speaking passengers. China Outbound is separate from the China JV Investment and wholly owned by us; |

| | CMV are to China Merchants Viking Cruises Limited, the entity of the China JV Investment that contracts with passengers and owns and operates the China JV Investments first ship; |

| | direct in relationship to the sales distribution channel are to passengers who purchased their cruise packages directly from us; |

| | Invested Capital are to the average of the most recent five quarters of indebtedness, gross of loan fees, plus total shareholders equity; |

| | large public cruise lines are to Carnival Corporation, Norwegian Cruise Line Holdings Ltd. and Royal Caribbean Cruises Ltd.; |

| | Net Promoter Score is to a metric that helps companies measure customer loyalty and that predicts overall company growth. Net Promoter Scores are measured through customer response to a single question on how likely they are to recommend the product or service to others and are reported with a number that ranges from -100 to +100. A higher score is more desirable, and score ranges tend to vary by industry. Vikings score is calculated by asking guests, How likely are you to recommend Viking Cruises to a friend? on a 0 to 10 scale. Percent 9 to 10 is calculated (as promoters), percent 7 to 8 is ignored (passives) and percent 0 to 6 (detractors) is calculated and subtracted from the percent of 9 to 10 scores. This results in a composite measure of share of promoters less share of detractors; |

| | Net Yield are to Adjusted Gross Margin divided by Passenger Cruise Days; |

| | NM are to certain metrics that were not meaningful and as such were excluded, including due to the impact of the novel coronavirus (COVID-19); |

| | North America and North American are to the United States of America and Canada; |

| | Occupancy are to the ratio, expressed as a percentage, of Passenger Cruise Days to Capacity Passenger Cruise Days with respect to any given period. Contrary to many of our competitors, we do not allow more than two passengers to occupy a two-berth stateroom. Additionally, we have guests who choose to travel alone and are willing to pay higher prices for single occupancy in a two-berth stateroom. As a result, our Occupancy cannot exceed 100%, and may be less than 100%, even if all our staterooms are booked; |

| | onboard revenue are to revenue generated during the course of a cruise and consists primarily of optional shore excursion revenue, onboard bar revenue and shop revenue; |

iii

Table of Contents

CONFIDENTIAL TREATMENT REQUESTED BY VIKING HOLDINGS LTD

PURSUANT TO 17 CFR 200.83.

| | Ongoing Capex are to investments in property, plant and equipment and intangible assets (PP&E), adjusted to exclude additions to PP&E for vessels and ships under construction and additions to PP&E for vessels and ships delivered in the relevant period; |

| | our core products are to Viking River, Viking Ocean, Viking Expedition and Viking Mississippi; |

| | our luxury ocean market share are to our share of capacity passengers of all ships operated by luxury ocean cruise lines (Atlas Ocean Voyages, Crystal Cruises, Emerald Cruises, Paul Gauguin Cruises, Regent Seven Seas Cruises, The Ritz-Carlton Yacht Collection, Scenic Luxury Cruises & Tours, Seabourn Cruise Line, SeaDream Yacht Club, Silversea Cruises and Windstar Cruises), and select small / medium size premium cruise lines that we consider direct competitors (Azamara and Oceania Cruises), which is sourced from Cruise Industry News, where capacity passengers is defined as the total number of passengers a ship can carry at 100% occupancy during a given time period, measured by sailing. Ocean cruise line passenger estimates include passengers on ships used for expedition cruises. As a result, our ocean market share includes our expedition ships; |

| | our North American outbound river market share are to our share of capacity passengers of brands that primarily service North American passengers on European waterways (AMA Waterways, Inc., Avalon Waterways, Emerald Cruises, Gate 1 Travel, Grand Circle Travel Corp., Tauck, Uniworld River Cruises, Inc., and Vantage Travel Service, Inc.), which is sourced from Cruise Industry News, where capacity passengers is defined as the total number of passengers a ship can carry at 100% occupancy during a given time period, measured by sailing; |

| | our primary source markets mean North America, the United Kingdom, Australia and New Zealand; |

| | outbound travel market are to the market of customers traveling internationally out of a particular country or continent; |

| | Passenger Cruise Days or PCDs are to the number of passengers carried for each cruise, with respect to any given period and for each ship operating during the relevant period, multiplied by the number of Ship Operating Days; |

| | pre- and post-trip cruise extension are to extensions available pre- and post-cruise. We also refer to our pre- and post-trip cruise extensions as land excursions; |

| | Premium Cruise Voucher are to vouchers generally with a face value of up to 125% of monies paid that we issued to guests when we cancelled sailings. Guests have generally had the option to receive either a refund in cash for 100% of monies paid or a Premium Cruise Voucher. Premium Cruise Vouchers can generally be applied to a new booking for up to two years from the voucher issuance date (or longer, if the expiration date is extended) and any unused Premium Cruise Vouchers are refundable for the original amount paid upon expiration; |

| | repeat guest percentage are, for any season, the percentage of North American passengers for that season who had traveled with us before; |

| | Return on Invested Capital or ROIC are to the ratio, expressed as a percentage, of operating income (loss) adjusted for income tax (expense) benefit divided by Invested Capital; |

| | Risk Free Vouchers are to vouchers issued under temporarily updated cancellation policies in response to the COVID-19 pandemic or other events creating travel uncertainty. Under these policies, guests who cancel their cruise have the option to receive Risk Free Vouchers instead of incurring cancellation penalties. Risk Free Vouchers can generally be applied to a new booking for up to two years from the voucher issuance date but are not refundable for cash; |

| | SCM are to Shenzhen China Merchants Viking Cruises Tourism Limited, the entity of the China JV Investment that provides services for business planning, management consulting, sales, product development and hotel operations to CMV; |

iv

Table of Contents

CONFIDENTIAL TREATMENT REQUESTED BY VIKING HOLDINGS LTD

PURSUANT TO 17 CFR 200.83.

| | season are to the respective calendar year for such season. For example, the 2023 season refers to the 2023 calendar year; |

| | Ship Operating Days are to the number of days within any given period that a ship is in service and carrying cruise passengers, determined on an aggregated basis for all ships in operation during the relevant period; |

| | shore excursions are to excursions provided at our destinations during a cruise itinerary; |

| | Total Debt are to indebtedness outstanding, gross of loan fees, excluding lease liabilities, Private Placement liabilities and Private Placement derivatives; |

| | VCL are to Viking Cruises Ltd, our direct wholly-owned subsidiary; |

| | Viking China are to our China Outbound product and the China JV; |

| | Viking Expedition are to our expedition cruise product marketed to our primary source markets; |

| | Viking Mississippi are to the river cruise product for cruising the Mississippi River marketed to our primary source markets; |

| | Viking Ocean are to our ocean cruise product marketed to our primary source markets; and |

| | Viking River are to our river cruise product marketed to our primary source markets. Viking Mississippi is a separate product from Viking River. |

v

Table of Contents

CONFIDENTIAL TREATMENT REQUESTED BY VIKING HOLDINGS LTD

PURSUANT TO 17 CFR 200.83.

TRADEMARKS AND DESIGNS

We have proprietary rights to trademarks used in this prospectus that are important to our business, many of which are registered under applicable intellectual property laws. Solely for convenience, trademarks and trade names referred to in this prospectus may appear without the ® or symbols, but such references are not intended to indicate, in any way, that we will not assert, to the fullest extent possible under applicable law, our rights or the rights of the applicable licensor to these trademarks and trade names. We do not intend our use or display of other companies trademarks, trade names or service marks to imply a relationship with, or endorsement or sponsorship of us by, any other companies. Each trademark, trade name or service mark of any other company appearing in this prospectus is the property of its respective holder.

vi

Table of Contents

CONFIDENTIAL TREATMENT REQUESTED BY VIKING HOLDINGS LTD

PURSUANT TO 17 CFR 200.83.

MARKET AND INDUSTRY DATA

We obtained the industry, market and competitive position data used throughout this prospectus from internal company surveys and management estimates, as well as from industry and general publications and research, surveys and studies conducted by third parties. We believe these internal company surveys and management estimates are reliable; however, no independent sources have verified such surveys and estimates. Third-party industry and general publications, research, studies and surveys generally state that the information contained therein has been obtained from sources believed to be reliable. None of the independent industry publications relied upon by us or otherwise referred to in this prospectus were prepared on our behalf. While we believe the industry, market and competitive position data included in this prospectus are reliable and are based on reasonable assumptions, these data involve many assumptions and limitations, and you are cautioned not to give undue weight to these estimates. We have not independently verified the accuracy or completeness of the data contained in these industry publications and other publicly available information.

Statements in this prospectus referring to Alter Agents refer to total and unaided brand awareness data collected for us on a quarterly basis since 2015 by Alter Agents Inc., a third-party leading market research firm, based on surveys of approximately 1,000 Americans aged 55 years and older who have cruised or traveled internationally within the past 5 years or have plans to do so in the next 3 years and expressed a willingness to cruise. Total brand awareness means the percentage of survey respondents who expressed knowledge of a specific brand when asked about that brand by name or when asked about general awareness of river cruising or ocean cruising, as applicable.

Certain estimates of market opportunity, forecasts or market growth and other forward-looking information included elsewhere in this prospectus involve risks and uncertainties and are subject to change based on various factors, including those discussed under Risk Factors, Special Note Regarding Forward-Looking Statements and Managements Discussion and Analysis of Financial Condition and Results of Operations.

vii

Table of Contents

CONFIDENTIAL TREATMENT REQUESTED BY VIKING HOLDINGS LTD

PURSUANT TO 17 CFR 200.83.

EXCHANGE CONTROL

Consent under the Exchange Control Act 1972 (and its related regulations) has been received. We intend to apply for and expect to receive consent under the Exchange Control Act 1972 (and its related regulations) from the Bermuda Monetary Authority for the issue and transfer of our securities to and between non-residents of Bermuda for exchange control purposes provided our ordinary shares remain listed on an appointed stock exchange, which includes the NYSE.

Pursuant to section 26 of the Companies Act 1981 of Bermuda (the Companies Act), there is no requirement for us to comply with Part IIIProspectuses and Public Offersof the Companies Act or to file this prospectus with the Registrar of Companies in Bermuda. Neither the Bermuda Monetary Authority, the Registrar of Companies of Bermuda nor any other relevant Bermuda authority or government body accept any responsibility for the financial soundness of any proposal or for the correctness of any of the statements made or opinions expressed in this prospectus.

viii

Table of Contents

CONFIDENTIAL TREATMENT REQUESTED BY VIKING HOLDINGS LTD

PURSUANT TO 17 CFR 200.83.

This summary highlights selected information contained elsewhere in this prospectus and does not contain all of the information that you should consider in making your investment decision. Before deciding to invest in our ordinary shares, you should read this entire prospectus carefully, including the sections of this prospectus titled Risk Factors, Special Note Regarding Forward-Looking Statements and Managements Discussion and Analysis of Financial Condition and Results of Operations and our financial statements included elsewhere in this prospectus.

BACKGROUND

Viking was founded in 1997 with four river vessels and a simple vision that travel could be more destination-focused and culturally immersive.

Today, we have grown into one of the worlds leading cruise lines, with a fleet of 92 small, state-of-the-art ships across our four products. From our iconic journeys on the worlds great rivers, including our new Mississippi River itineraries, to our ocean voyages around the globe and our extraordinary expeditions to the ends of the earth, we offer meaningful travel experiences on all seven continents in all three categories of the cruise industryriver, ocean and expedition cruising.

1

Table of Contents

CONFIDENTIAL TREATMENT REQUESTED BY VIKING HOLDINGS LTD

PURSUANT TO 17 CFR 200.83.

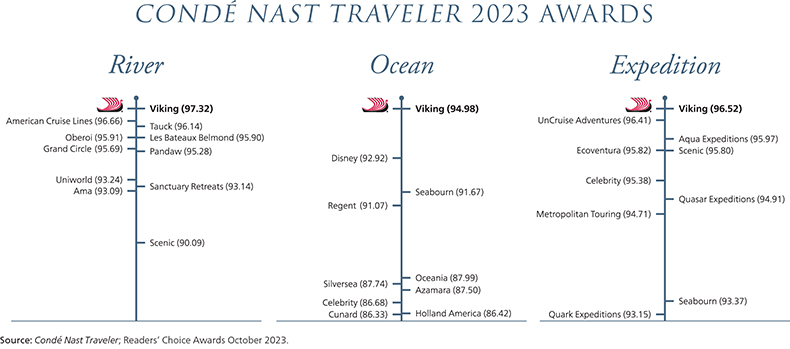

With more than 450 awards to our name, we are a leader in the industry and were rated #1 for Rivers, #1 for Oceans (for ships sized 500 to 2,500 berths) and #1 for Expeditions by Condé Nast Traveler in the 2023 Readers Choice Awards. This is the first time a travel company has been voted #1 in all three categories simultaneously.

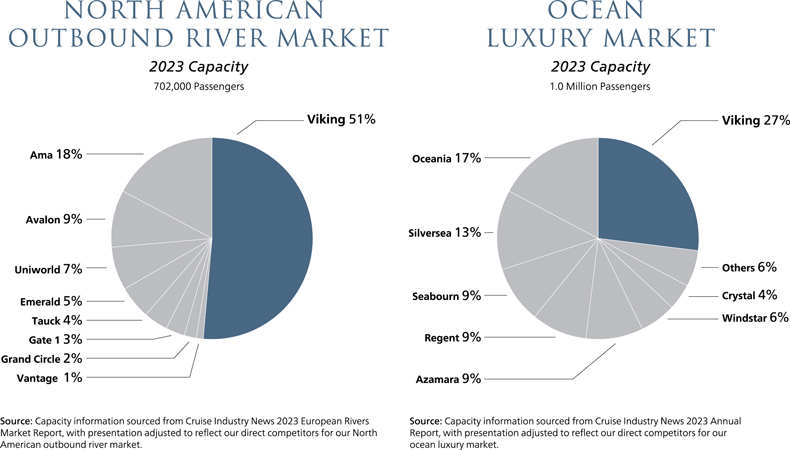

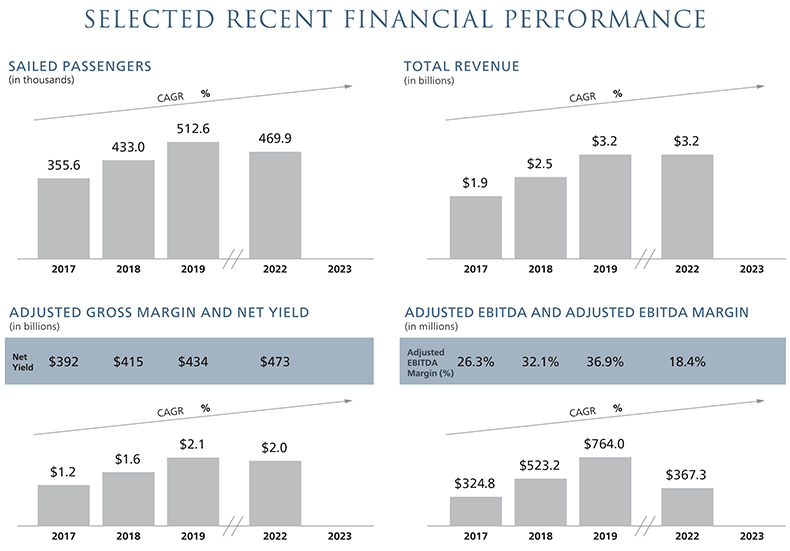

We have generated rapid growth driven by strong demand for our products and a highly differentiated guest experience, resulting in industry-leading capacity growth and the proven ability to expand our travel platform with new destinations and experiences. From 2015 to 2023, our total number of guests, total revenue, net income and Adjusted EBITDA grew at CAGRs of %, %, % and %, respectively. We have grown faster than the overall cruise industry since 2015 to become the market leader in river cruising and luxury ocean cruising, demonstrating our ability to succeed in each new category we have entered. For the 2023 season, our North American outbound river market share was 51% and our luxury ocean market share was 27%.

2

Table of Contents

CONFIDENTIAL TREATMENT REQUESTED BY VIKING HOLDINGS LTD

PURSUANT TO 17 CFR 200.83.

For the year ended December 31, 2023, guests traveled with us, and we generated $ billion of total revenue, $ million of net income and $ million of Adjusted EBITDA. See Summary Consolidated Financial and Other Data for additional information about Adjusted EBITDA, including a reconciliation of Adjusted EBITDA to net income. As of December 31, 2023, we had $ billion of cash and cash equivalents and $ billion of Total Debt. We have also generated industry-leading ROIC at % for the year ended December 31, 2023.

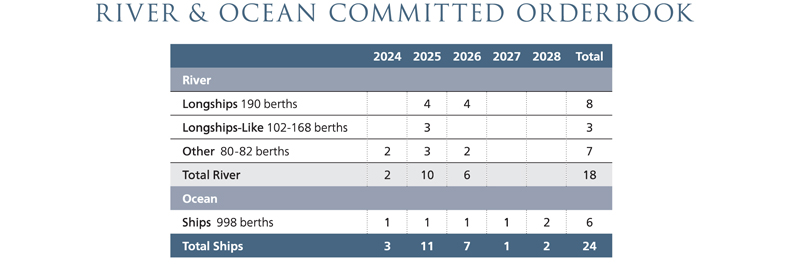

We believe we are well-positioned for future growth. To address the strong demand from our guests, we have ordered 18 new river vessels for delivery through 2026 and six new ocean ships for delivery through 2028.

THE VIKING DIFFERENCE

1. One Brand: Among our guests and across the industry, the Viking brand is synonymous with excellence. Our guests can experience all three categories of the cruise industryocean, river and expedition cruising under our single brand. Rather than creating a conglomerate of different brands, all of our products are a consistent extension of the Viking brand. As a result, our marketing spend and strong brand loyalty drive growth for all of our products. We also leverage our strong brand loyalty for future product launches, with over 60% of bookings for each of the inaugural seasons for Viking Ocean, Viking Expedition and Viking Mississippi made by past guests. Our guests know they can expect a consistent, excellent experience on each voyage they take with us, which has allowed us to expand our travel platform successfully with new destinations and experiences. For the 2023 season, our repeat guest percentage was 51%.

2. Identical Small Ships: Our fleet includes 58 identical Longships accommodating 190 passengers, nine identical ocean ships accommodating 930 passengers and two identical expedition ships accommodating 378 passengers. Within each product, our ships are indistinguishable to our guests. This simplifies the sales and marketing process as potential guests shop by itinerary versus by specific ship or age of ship, and it allows older ships to achieve similar yields, even when introducing new ships. Identical ships also create operational flexibility, as well as efficiencies around shipbuilding, maintenance and crew, which improves our margins. Our small ships can dock in ports where larger ships cannot, providing our guests more time ashore for cultural discovery and exploration and offering our guests experiences they cannot have with other cruise lines.

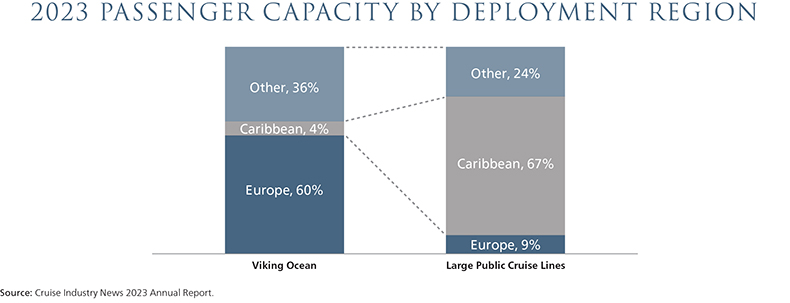

3. Clearly Defined, Destination-Focused Experience: We are the only cruise line offering experiences on all seven continents with itineraries across five oceans, 21 rivers and five lakes, and a focus primarily on destinations in Europe and the Mediterranean, rather than the Caribbean. We deliver a highly differentiated experience for our guests by prioritizing exploration of the destination versus onboard consumption and traditional entertainment. The Viking experience is well-defined and all-inclusive, with a shore excursion included in every port. We are also known for the things that we do not do. For example, no children under 18, no casinos and no hidden ancillary costs, such as charges for alternative restaurants, wi-fi or beer and wine at lunch and dinner. Because of these strategic choices, our guests instantly recognize the Viking way of travel.

3

Table of Contents

CONFIDENTIAL TREATMENT REQUESTED BY VIKING HOLDINGS LTD

PURSUANT TO 17 CFR 200.83.

4. Clear Customer Focus: We are intently focused on the travel needs of our core demographic of curious, affluent, English-speaking travelers aged 55 years and older, which is an attractive segment of the travel market. We believe we know our core demographic better than anyone else in the industry and we have tailored our products to specifically address the travel needs of the Thinking Person. We attract individuals seeking travel experiences that offer cultural insight and personal enrichment.

5. Strong Direct Marketing: Since 1997, we have invested $2.5 billion in all aspects of marketing, most of which is direct marketing spend. This investment has helped build and solidify the value of our brand with our target market. Our marketing database includes more than 56 million North American households, including 1.5 million households that have traveled with us before. We generate our own demand through our direct marketing, which allows us to obtain industry-leading early booking rates. Our marketing also drives direct bookings. For the year ended December 31, 2023, more than 50% of our guests booked directly with us.

6. Only Pure-Play Luxury Public Cruise Line: Viking will be the only pure-play luxury public cruise line. In contrast, the large public cruise lines have multiple brands that serve all three categories of the cruise market, with luxury representing only a small percentage of their overall capacity. Our total revenue per passenger was $ for the year ended December 31, 2023. Viking defines the luxury category of the river cruise and ocean cruise markets. We believe these are the most attractive segments of the cruise industry and the global luxury leisure travel market given their growth potential.

VIKING STRENGTHS

We have several strengths that have propelled our success and distinguished us from other travel businesses.

High quality products drive strong guest satisfaction and brand loyalty.

We have a proven track record of delivering high quality travel experiences that resonate with our guests, driving strong guest satisfaction and brand loyalty. As a result, our guests are often our greatest promoters. For the 2023 season, as of December 31, 2023, our Net Promoter Scores were 70 for Viking River and 63 for Viking Ocean. Based on our 2023 season survey, on a scale of 0 to 10, 78.0% and 73.5% of our Viking River and Viking Ocean guests, respectively, answered 9 or 10 on likelihood of recommending Viking to a friend.

Our strong guest satisfaction and brand loyalty drive repeat bookings with Viking. For the 2023 season, our repeat guest percentage was 51%, and more than 50% of our guests booked directly with us. Our new product

4

Table of Contents

CONFIDENTIAL TREATMENT REQUESTED BY VIKING HOLDINGS LTD

PURSUANT TO 17 CFR 200.83.

launches have also experienced overwhelming support from our past guests, with over 60% of bookings for each of the inaugural seasons for Viking Ocean, Viking Expedition and Viking Mississippi made by past guests. We have also seen comparable booking trends by past guests for the launch of new river itineraries in Egypt and Vietnam. Our guests trust us to create best-in-class travel experiences, whether it be a new itinerary for a product they already love or a completely new product experience, and we leverage our strong bookings for future seasons and our robust customer insights practice to help identify and deliver on the needs of our core demographic. Expanding our travel platform enables us to capture a greater portion of our core demographics travel spend, while reinforcing brand loyalty, building customer lifetime value and increasing our repeat guest percentage, all of which generate shareholder value.

Single Viking brand drives awareness.

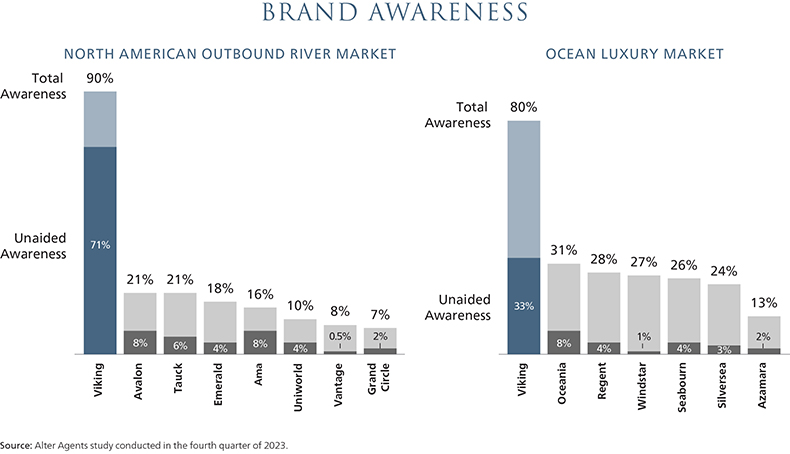

For the past 26 years, we have built a single Viking brand that is highly recognized in our target markets and around the world. Today, we are the leading brand in the North American outbound river market and the luxury ocean market. As of December 31, 2023, we had 90% and 80% total brand awareness for river cruises and ocean cruises, respectively, among our target demographic in the United States, according to a study by Alter Agents.

With a single Viking brand, our strong brand awareness drives growth for our entire travel platform as all of our products are a consistent extension of the Viking experience. We are also able to streamline our marketing, with word-of-mouth marketing and traditional marketing spend driving brand awareness and growth for all of our products.

Clear customer focus on an attractive demographic.

We are intently focused on our core demographic of curious, affluent travelers aged 55 years and older, which we believe is an attractive segment that has been and continues to be underserved by the travel market.

5

Table of Contents

CONFIDENTIAL TREATMENT REQUESTED BY VIKING HOLDINGS LTD

PURSUANT TO 17 CFR 200.83.

The U.S. population aged 55 years and older comprises 30% of the total population, has the largest spending power of any demographic based on annual expenditures and holds over 65% of U.S. wealth as measured by the U.S. Federal Reserve. The U.S. population aged 55 years and older is also the fastest growing segment of the population, with expected growth from 98 million people in 2020 to 109 million people in 2030, according to the Congressional Budget Office. Our target demographic has greater financial stability, which can make them more resilient to economic conditions and more willing to invest in high-quality travel experiences, including luxury accommodations, unique excursions and cultural activities. Our target demographic often appreciates comfort, convenience and experiential travel that provides a balance between adventure and luxury. Many of our guests are also retired or approaching retirement, which means they often have flexible schedules that allow them to book earlier and plan for extended travel.

After 26 years, we believe we know our core demographic better than anyone else in the industry and have tailored our products to specifically address their unmet needs in the broader travel market. Leveraging our robust customer insights practice and two decades of experience, we know what our guests expect in their travelsa calm onboard atmosphere, with a destination-focused experience offering cultural or scientific enrichment. Our guests spend their time enjoying the peaceful ambiance of resident musicians, participating in enriching educational opportunities, such as onboard lectures from local historians, or debriefing their exciting day with fellow guests over a delicious meal from the ships regional specialties menu. At Viking, we think of every detail, so our guests can focus on exploring and learning about their destinations.

Data-driven marketing platform drives demand.

Since 1997, we have invested $2.5 billion across all aspects of marketing. We became a national corporate sponsor of PBSs Masterpiece Theatre in 2011 when Downton Abbey was on the air, establishing Viking as a household name, and we continue to run television advertisements on other national programming targeting our core demographic. We have forged partnerships with prestigious cultural institutions, such as the Metropolitan Opera, TED and the Los Angeles Philharmonic. We also created Viking.tv, one of the travel industrys most extensive libraries of online content. This award-winning free enrichment channel was initially conceived to maintain daily contact with our guests during the COVID-19 pandemic, and continues to stream daily, with over 1,000 unique episodes since first airing. Additionally, we host hundreds of journalists and influencers on board our ships each year, generating robust earned media coverage and social media content. These efforts create a clear path for positive affiliation with the Viking brandhelping move guests from awareness into consideration.

Built over the last 26 years, our marketing database includes more than 56 million North American households, including 1.5 million households that have traveled with us before. While we have always relied on traditional marketing strategies, including direct mail, TV, print and trade marketing, our marketing approach today is omnichannel, with robust digital capabilities and data-driven decision-making. For example, our marketing is underpinned by digital industry tools that provide programmatic execution, machine learning capabilities, look-alike prospecting, online to offline conversions and call tracking, emerging artificial intelligence (AI) supported functionality and data-driven marketing attribution. The households in our database are modeled and scored for their propensity to book. These scores, combined with our attribution systems and a robust consumer insights practice, direct how we tailor our marketing in order to meet consumers where they are, with the right message at the right time. We also continue to shift our marketing spend towards digital channels.

Once guests travel with us, our marketing positioning is reinforced by a shared experience among individuals seeking travel experiences for the Thinking Person. Our guests connect with each other over mutual interests in history, art, culture and travel, and as a result, countless new friendships are forged on board our ships each year. Approximately 18% of our Viking Ocean and Viking Expedition guests booked their next Viking voyage while on board in 2023with many planning future trips together with fellow travelers. And, just like the fervent communities formed around beloved books and films, guests self-described as hooked on Viking have

6

Table of Contents

CONFIDENTIAL TREATMENT REQUESTED BY VIKING HOLDINGS LTD

PURSUANT TO 17 CFR 200.83.

launched their own fan groupsseveral of which have amassed more than 40,000 memberson social media platforms where we are able to target them with digital marketing for their next Viking voyage.

Significant direct bookings optimize yields and improve margins.

We provide our guests with a variety of ways to seamlessly book their voyages, so that they can transact with us however they are most comfortable. Guests can book directly with Viking through multiple outlets, including our website, via online chat with an agent, over the phone, or on board our ships that have a dedicated travel consultant. Guests also have the option to book with a third-party travel agent. By offering multiple channels to serve our guests, we reduce friction in the booking process and increase our direct bookings, which optimizes yields and improves margins. We also believe our strong direct marketing capabilities drive earlier direct bookings, including during times of softening demand in the broader travel market.

For the year ended December 31, 2023, more than 50% of our guests booked directly with us. Direct bookings reduce commissions paid to travel agents and improve our margins. Direct bookings also provide an additional opportunity for direct contact with our guests, allowing us to build stronger brand awareness and deliver a more personalized experience for our guests. With a marketing database that includes more than 56 million North American households, we believe our direct bookings will continue to grow and add value to our business.

Early bookings create strong revenue visibility and facilitate long-term planning.

For the 2024 season, we began selling select itineraries more than two years prior to the start of the season. On average for the 2023 season, our guests booked eleven months in advance. By generating early demand through our direct marketing, we believe we attain bookings earlier than the large public cruise lines. Additionally, we collect payment earlier than the large public cruise lines, which we believe reduces cancellations. This creates future revenue visibility, which enables us to better manage our capacity and pricing. This visibility also gives us the ability to plan for future ship commitments years in advance.

We have a proven track record of selling Capacity PCDs well in advance of sailing. With additional newbuilds delivered and new products launched, we grew Capacity PCDs for our core products from 3.3 million in 2017 to 6.7 million in 2024, a CAGR of 10.6%. Even with this growth, we continue to enter every season with a high percentage of Capacity PCDs booked. For the 2017 season, 63.7% of Capacity PCDs for our core products were booked as of December 31, 2016, which increased to 73.9% of Capacity PCDs for our core products booked for the 2024 season as of December 31, 2023. Entering a season with over 70% of Capacity PCDs sold provides significant revenue visibility, allowing us to focus our marketing efforts on selling future seasons earlier than competitors and continuing the cycle of strong Advance Bookings.

For our core products, operating capacity is 34% higher for the 2023 season in comparison to the 2019 season and 4% higher for the 2024 season in comparison to the 2023 season. For our core products as of November 12, 2023, for the 2023 and 2024 seasons, we had sold 95% and 68%, respectively, of our Capacity PCDs and had $4,067 million and $3,459 million, respectively, of Advance Bookings. For our core products as of November 12, 2023, Advance Bookings per PCD for the 2023 season was $672, 12.1% higher than the 2019 season, and Advance Bookings per PCD for the 2024 season was $762, 8.1% higher than the 2023 season.

Young fleet with innovative design drives efficiency and profitability.

At Viking, we build innovative ships that are the right size for the experience. From the outset, we creatively balance competing preferences for smaller ships and spacious, uncrowded shared areas through greater efficiencies in space utilization and operations. No space is wasted onboard, and the overall ship design thoughtfully optimizes efficiency and profitability. For example, for Viking Ocean, the layout of our ships allows us to operate with fewer crew while still delivering an exemplary level of service. And for Viking River, the unique design of our Longships allows us to comfortably accommodate approximately 20% more guests than typical European river vessels, improving the profitability of our vessels.

7

Table of Contents

CONFIDENTIAL TREATMENT REQUESTED BY VIKING HOLDINGS LTD

PURSUANT TO 17 CFR 200.83.

As part of our approach to fleet design, our Viking Ocean, Viking Expedition and the majority of our Viking River fleet are identical at the product level, which provides us with many benefits. This simplifies the sales and marketing process as potential guests shop by itinerary versus by specific ship or age of ship and allows older ships to achieve similar yields, even when introducing new ships. From an operational perspective, fleet commonality creates efficiencies around maintenance, as spare parts can be purchased in bulk in advance for unforeseen or planned maintenance, and crew, as crew can be moved around the fleet with minimal additional training. Lastly, our identical fleet gives us operational flexibility to interchange guests between ships in the event of unexpected disruptions, such as when we positioned identical Longships on adjacent sides of low water areas to avoid any cancellations during record low water levels in Europe in 2022.

We also have one of the youngest fleets in the industry. As of December 31, 2023, the average age for our fleet was seven years, which is younger than the average age for the large public cruise lines. We believe customers are willing to pay a premium to sail on newer ships, which results in higher yields. A young fleet also has more efficient operations, including from technological advances that result in lower fuel consumption, resulting in stronger margins. A young fleet also requires lower maintenance capital expenditures, which allows us to direct most of our capital expenditures to fleet expansion and the launch of new product offerings, which ultimately means that more of our capital is invested in initiatives designed to grow our revenue and cash flows as opposed to maintaining revenue and cash flows at current levels.

Fuel-efficient fleet designed to meet future environmental regulations.

From the outset, we have designed all of our ships thoughtfully to reduce their fuel consumption, carbon footprint and overall environmental impact. Our Longships are one of the first cruise vessels to be voluntarily certified with the Green Award and the European ISO 14001 Environmental Management practices. Our ocean ships, with their sleek hull design and closed-loop scrubbers that allow us to use more cost-efficient fuel, exceed the current requirements of the International Maritime Organization (IMO) Energy Efficiency Design Index (EEDI) by approximately 25%, and will exceed the 2025 EEDI requirements by almost 20%. Our expedition ships set a new standard for responsible travel by exceeding the current requirements of the EEDI by nearly 38%. Due to the design choices across our fleet, our fuel costs represented only % of our total revenue for the year ended December 31, 2023, favorably positioning us if fuel prices increase or regulations require the use of more expensive fuel types. With only minor modifications, the engines of our Longships, ocean ships, and expedition ships can also operate on hydrotreated vegetable oil (HVO) renewable diesel, which could reduce greenhouse gases by up to 90% over the fuels life cycle compared to diesel.

Looking forward, our next generation of ocean ships, beginning with Ship XIII to be delivered in 2026, will be our most environmentally friendly ships with hydrogen fuel cells on board. We have made the principled decision not to invest in liquid natural gas (LNG), which is composed almost exclusively of methane, a greenhouse gas with a global warming potential more than 80 times (over a 20-year period) or 28 times (over a 100-year period) that of carbon dioxide. Instead, we believe onboard hydrogen fuel cells will allow us to meet future environmental regulations on fuel consumption and operate at zero-emission in the Norwegian Fjords and other sensitive environments. While we plan to continue to use traditional fuel to operate our standard itineraries in the near term, our ocean ships are well-positioned to increase their use of hydrogen as the supply chain improves.

Seasoned, proven management team committed to long-term shareholder value.

We are a founder-led and inspired organization with an enduring commitment to creating shareholder value over the long-term. In addition to Torstein Hagen, our Chairman and Chief Executive Officer, we benefit from the industry expertise and tenure of our proven management team of Leah Talactac, our Chief Financial Officer, Linh Banh, our Executive Vice President, Financial Planning and Analysis, Jeff Dash, our Executive Vice President, Head of Business Development, Karine Hagen, our Executive Vice President, Product, Anton

8

Table of Contents

CONFIDENTIAL TREATMENT REQUESTED BY VIKING HOLDINGS LTD

PURSUANT TO 17 CFR 200.83.

Hofmann, our Executive Vice President, Operations, Milton Hugh, our Executive Vice President, Sales and Richard Marnell, our Executive Vice President, Marketing, who have all worked together for over 15 years.

Excluding our Chairman and Chief Executive Officer, our management team has an average tenure of 20 years at Viking and 24 years in the travel industry. The same management team revolutionized the river cruising industry with the design and launch of the Longships in 2012, and introduced Viking Ocean in 2015, which marked the industrys first entirely new ocean cruise line in nearly a decade. This team identified a market need for a smaller ship, destination-focused ocean product, which continues to be a key driver in our growth. More recently, this team launched Viking Expedition and Viking Mississippi in 2022, meeting guest demands. Along with launching new products, this team has also been successful in broadening our presence in existing source markets and garnering leading market share and entering new source markets, such as China. From 2020 to 2023, this team also added 18 new ships to our fleet, including 11 river vessels, four ocean ships, two expedition ships and the Viking Mississippi. This team has driven our growth over the past two decades, with a % increase in our annual guests growing from 80,000 in 2007 to over in 2023. This team also has a proven record of capitalizing on opportunities as they arise. For example, given our long-term outlook, we have a record of ordering newbuilds, including our initial ocean ships, during off cycles when other cruise operators focused on conserving capital. Currently, we have ordered 24 additional newbuilds through 2028 to capture future demand.

Our management team has capitalized on opportunities during times of adversity, weathered several economic cycles together and ultimately built Viking to be the company it is todaya household brand name with industry-leading quality ratings, numerous awards and a sizeable market share in the fast-growing luxury cruise market.

Dedicated crew delivers exemplary level of service.

Our crew, with over 10,000 crewmembers from over 90 different countries at the peak of the 2023 season, are dedicated to making our guests journeys as memorable as possible. Our crew is essential to our success. Our crews friendliness, attentiveness and attention to detail have garnered us more consumer and industry awards than any other travel company on rivers or oceans. Most importantly, our crew is a significant reason that we receive high satisfaction ratings from our guests.

As part of the Viking family, we care deeply about our crew, and we provide the training, skills and resources needed for them to excel. Our proprietary training program, Viking College, helps our crew learn and grow. We also place great value on promotion from within, rewarding hard work, enthusiasm, initiative and a sense of responsibility and ownership. We aspire to be the employer of choice among cruise lines and our crew retention rate of about 80% is a source of great pride. Retaining our crew season after season lowers our recruiting and training costs. It also supports our growthwe are able to distribute our tenured crew across our new ships to streamline the hiring and training of new crew. A mix of new and tenured crew on each ship ensures a consistent high quality of service and a familiar onboard experience for our guests as we grow our business.

VIKING STRATEGIES FOR GROWTH

We believe our journey as one of the most recognized luxury travel brands in the world is just beginning. We believe we are well-positioned to drive future growth and profitability with the following strategies, each of which represents a continuation of the proven strategies we have been executing over the past 26 years.

Expand our fleet to address unmet demand from our core demographic.

We believe the travel market for curious, affluent travelers aged 55 years and older continues to be significantly underserved. There is also a general gap between demand and supply in cruising, which we have an opportunity to address.

9

Table of Contents

CONFIDENTIAL TREATMENT REQUESTED BY VIKING HOLDINGS LTD

PURSUANT TO 17 CFR 200.83.

To capitalize on this growing and unmet demand, we plan to continue expanding our fleet, with the most contracted future ship deliveries in the industry. According to Cruise Industry News, approximately 14% of total new berths coming online globally by 2028 are attributable to ships with fewer than 1,000 berths and our contracted capacity represents approximately 39% of this new comparable supply, positioning us favorably to take advantage of increased demand for cruising within our target market. For Viking River, we have ordered 18 new vessels for delivery by 2026, including 11 river vessels for the European rivers, six river vessels that will operate in Egypt and a chartered river vessel that will travel through Vietnam and Cambodia, and we expect to

sustain our market leading position in the river cruising market well into the future. For Viking Ocean, we believe there is significant future growth potential, which we will begin to achieve with six new ocean ships on order for delivery through 2028. We also have options for four additional ocean newbuilds, with two for delivery in 2029 and two for delivery in 2030. Our orderbook is driven by a disciplined strategy that relies heavily on robust consumer insights and market demand assessment, combined with financing and yield considerations.

As we add new capacity, we conduct extensive research to identify new itineraries that will fill gaps in the travel market for our core demographic. Based on prior experience, we expect new itineraries to inspire past guests to travel again and attract new guests to the Viking brand, which we believe will result in a higher repeat guest percentage and enhanced customer lifetime value at marginal marketing expense.

In addition to growing our fleet and adding new itineraries, we also plan to continue optimizing our inventory of add-on products, such as pre- and post-trip cruise extensions, which unlock additional revenue growth opportunities without significant capital expenditures. Our pre- and post-trip cruise extensions, such as a three-night tour of the historic town of Oxford and Highclere Castle or the real Downton Abbey, further enrich the destination-focused experience of our itineraries and provide another opportunity for us to connect our guests with the cultures and destinations on our itineraries. In 2023, over 45% of our guests purchased a pre- or post-trip cruise extension to take advantage of these opportunities. Pre- or post-trip cruise extensions are currently offered at an average of over $900 per extension and are typically two or three days.

Increase guests from outside of North America.

North America is the largest source market for the cruise industry and for Viking. For the year ended December 31, 2023, % of our guests came from North America, with the remainder primarily coming from the United Kingdom, Australia and New Zealand. We believe there is significant unmet demand for our core products in the United Kingdom, Australia and New Zealand. We also believe there is an opportunity to source guests for our core products from other markets, such as India, Singapore and the Nordic countries. In order to provide a seamless experience for our guests, all of our onboard and onshore programming is offered in a

10

Table of Contents

CONFIDENTIAL TREATMENT REQUESTED BY VIKING HOLDINGS LTD

PURSUANT TO 17 CFR 200.83.

singular language. For our core products, all programming is in English and for our China Outbound product, all programming is in Mandarin.

Continue to expand Viking China and launch products for new source markets.

The Chinese market is a large source for leisure travel. According to the World Bank and the Cruise Lines International Association (CLIA), there were 154.6 million international departures from China in 2019 and 1.9 million passengers from China traveled on a cruise line in 2019. According to a leading global consulting firm, while the Chinese outbound market has been slower to rebound from the COVID-19 pandemic, Chinese tourists maintain a strong desire to travel internationally, and outbound travel is expected to increase in 2024.

In 2016, we brought our brand of curiosity-driven travel to the Chinese source market by launching China Outbound, a river cruise experience in Europe with 100% Mandarin-speaking crew, and food, entertainment and excursions completely dedicated to Chinese guests. As a result, we believe we are uniquely positioned to capitalize on the Chinese market, which represents a continued opportunity for growth. Mandarin-speaking travelers in China, as well as other Asian-source markets, have been historically underserved by the cruise industry and we have identified a sizeable addressable market. We believe we are the only cruise line with a product dedicated to Mandarin-speaking guests in Europe and the launch of China Outbound in 2016 was just the beginning. By leveraging our brand awareness in China and our extensive research into the travel preferences of affluent Mandarin-speaking guests, we plan to continue to develop China Outbound, with the possibility of growing the fleet or expanding to include other offerings, such as ocean cruising. For coastal cruising in China, the China JV Investments Zhao Shang Yi Dun has a competitive advantage in the upper premium cruise line space as it is the only modern cruise ship currently in this market.

There are also opportunities to bring our brand of curiosity-driven travel to other source markets. Similar to China Outbound, new source markets provide an exciting opportunity to tailor our existing products exclusively to these source markets, while leveraging our experience building our core products with a singular language and potentially using a portion of our existing fleet.

Strategically expand our product portfolio.

We believe we can harness our global travel expertise, our experienced operational team and deep understanding of our core demographic to further expand our platform. Based on our robust customer insights practice and third-party research, we believe there is considerable demand for other Viking products from our past guests, as well as from our broader core demographic. In particular, we believe there is significant future opportunity to create dedicated land-based products given the strong demand for our pre-and post-trip extensions. As our guests generally enjoy multiple forms of travel and take multiple trips per year, land-based product offerings would meet an additional portion of the travel needs of our core demographic. This would enable us to capture a greater share of our guests travel spend and extend our customer lifetime value and connection to the Viking brand.

FINANCIAL PERFORMANCE

Our financial performance reflects the growing demand for our products, our strong capacity growth and the benefits of our loyal customer base. Our loyal guests book their journeys well in advance, and as a result, we have industry-leading early booking rates, which give us a competitive advantage in allocating capacity, optimizing pricing, managing yield and planning for future ship commitments years in advance. As a result, we are able to generate high margins and industry-leading ROIC. For the year ended December 31, 2023, our ROIC was %. We have also historically generated substantial Adjusted FCF that we have reinvested in our business to support growth. For the year ended December 31, 2023, we generated $ million of Adjusted FCF, which

11

Table of Contents

CONFIDENTIAL TREATMENT REQUESTED BY VIKING HOLDINGS LTD

PURSUANT TO 17 CFR 200.83.

translates to an Adjusted FCF Conversion of %. See Summary Consolidated Financial and Other Data for additional information about ROIC and Adjusted FCF, including a calculation of ROIC and a reconciliation of cash flows from (used in) operating activities to Adjusted FCF. Our strong balance sheet provides flexibility to finance future growth at attractive terms. As of December 31, 2023, we had $ billion of cash and cash equivalents and $ billion of Total Debt.

Like all other companies in the travel industry, our operations were impacted by the COVID-19 pandemic. In March 2020, we were the first cruise line to halt operations. From that point on, we spent significant resources implementing new health and safety protocols, including adding onboard testing laboratories on our ocean and expedition ships. These investments allowed us to restart operations in May 2021, with more than half of our river fleet and all six of our ocean ships operating at the peak of the 2021 season.

By 2022, more of our guests were traveling again. In 2022, 469,935 guests traveled with us, with an Occupancy of 78.4%, and in 2023, guests traveled with us ( % more than 2019), with an Occupancy of %. We believe our nimble operations, our experienced, cohesive management team and our consistent execution distinguishes us from other travel businesses and accelerated our recovery, both on a total revenue and an Adjusted EBITDA basis, in comparison to the large public cruise lines.

This strategy resulted in the following results from 2017 to 2023:

| | Total revenue increased from $1.9 billion during the year ended December 31, 2017 to $ billion during the year ended December 31, 2023. |

| | Gross margin increased from $0.6 billion in 2017 to $ billion in 2023. |

| | Adjusted Gross Margin increased from $1.2 billion during the year ended December 31, 2017 to $ billion during the year ended December 31, 2023. |

| | Net income increased from a net loss of $55.1 million during the year ended December 31, 2017 to net income of $ million during the year ended December 31, 2023. Net income includes the impact of the Private Placement derivative gain (loss) and interest expense related to our Series A Preference Shares, Series B Preference Shares and Series C Preference Shares, as applicable. Our Series A Preferences Shares and Series B Preference Shares are no longer outstanding. Our Series C Preference Shares will automatically convert into ordinary shares immediately prior to the consummation of this offering. |

| | Adjusted EBITDA and Adjusted EBITDA Margin increased from $324.8 million and 26.3%, respectively, during the year ended December 31, 2017 to $ million and %, respectively, during the year ended December 31, 2023. |

12

Table of Contents

CONFIDENTIAL TREATMENT REQUESTED BY VIKING HOLDINGS LTD

PURSUANT TO 17 CFR 200.83.

See Summary Consolidated Financial and Other Data for additional information about Adjusted Gross Margin and Adjusted EBITDA, including a reconciliation of Adjusted Gross Margin to gross margin and a reconciliation of Adjusted EBITDA to net income.

RISK FACTORS

Investing in our ordinary shares involves substantial risks, and our ability to successfully operate our business and execute our growth plan is subject to numerous risks. You should carefully consider the risks described in Risk Factors before making a decision to invest in our ordinary shares. If any of these risks actually occur, our business, financial condition or results of operations could be materially and adversely affected. In such case, the trading price of our ordinary shares would likely decline, and you may lose all or part of your investment. These risks include, among others, the following:

| | Changes in the general worldwide economic and political environment could reduce the demand for cruises. |

| | Adverse weather conditions or other natural disasters, including high or low river water levels, may require us to alter our itineraries or cancel existing cruises. |

| | Adverse incidents involving cruise ships may adversely affect our business, financial condition and results of operations. |

| | Disease outbreaks or pandemics have had, and in the future could have, a significant impact on the travel industry generally and on our business and results of operations. |

| | The threat of terrorist attacks, wars, acts of piracy and other events affecting the safety and security of travel can reduce the demand for cruises or require us to cancel existing bookings. |

13

Table of Contents

CONFIDENTIAL TREATMENT REQUESTED BY VIKING HOLDINGS LTD

PURSUANT TO 17 CFR 200.83.

| | Changes in fuel prices would affect the cost of our cruise ship operations and our hedging strategies may not protect us from increased costs related to fuel prices. |

| | Increased labor costs or our inability to recruit or retain employees may adversely affect our business, financial condition and results of operations. |

| | Increases in inflation could adversely affect our business, financial condition and results of operations. |

| | Fluctuations in foreign currency exchange rates could affect our financial results. |

| | An increase in cruise capacity without a corresponding increase in demand and infrastructure could adversely affect our business, financial condition and results of operations. |

| | Our success is substantially dependent on the continued service of our senior management. |

| | Our expansion into new products may be unsuccessful. |

| | Conducting business internationally may result in increased costs and risks. |

| | If we experience delays in ship construction or ship repairs, maintenance or refurbishments or changes in costs, our business, financial condition and results of operations could be adversely affected. |

| | Lack of continuing availability of attractive, convenient and safe port destinations could adversely affect our business, financial condition and results of operations. |

| | We rely on travel agencies to generate a material portion of our sales. |

| | Reductions in the availability of and increases in the prices for the services and products provided by our vendors could adversely affect our business and revenues. |

| | We rely on scheduled commercial airline services to transport our guests to or from the cities where our cruises embark and disembark. |

| | Credit card processing terms and requirements, adverse changes in guest payment policies, and consumer protection legislation or regulations could negatively affect our financial condition. |

| | The Viking name and brand are integral to the success of our business. |

| | Breaches in data security or other disturbances to our information technology systems and networks and operations could adversely affect our business, financial condition and results of operations. |

| | We are highly leveraged. We have substantial indebtedness and we may not be able to generate sufficient cash to service all of our indebtedness or to obtain additional financing if necessary. |

| | We are subject to complex laws and regulations, including environmental laws and regulations. |

| | Amendments to existing tax laws, rules or regulations or enactment of new unfavorable tax laws, rules or regulations could have an adverse effect on our business and financial performance. |

CORPORATE INFORMATION

Viking Holdings Ltd is incorporated in Bermuda as an exempted company. Our registered office is located at Clarendon House, 2 Church Street, Hamilton HM 11, Bermuda, and our principal executive offices are located at 94 Pitts Bay Road, Pembroke, Bermuda HM 08. Our telephone number is (441) 478-2244. We maintain the following website: www.viking.com. Our website provides information about our ships, itineraries and bookings. However, information contained on our website is not incorporated by reference in or otherwise a part of this prospectus. We have included our website address in this prospectus solely for informational purposes.

14

Table of Contents

CONFIDENTIAL TREATMENT REQUESTED BY VIKING HOLDINGS LTD

PURSUANT TO 17 CFR 200.83.

IMPLICATIONS OF BEING A FOREIGN PRIVATE ISSUER

Upon the consummation of this offering, we will report under the Securities Exchange Act of 1934, as amended (the Exchange Act), as a foreign private issuer. As a foreign private issuer, we may take advantage of certain provisions under NYSE rules that allows us to follow Bermuda law for certain corporate governance matters. As long as we continue to qualify as a foreign private issuer under the Exchange Act, we will be exempt from certain provisions of the Exchange Act that are applicable to U.S. domestic public companies, including:

| | the rules under the Exchange Act requiring domestic filers to issue financial statements prepared under U.S. generally accepted accounting principles (GAAP); |

| | the sections of the Exchange Act regulating the solicitation of proxies, consents or authorizations with respect to a security registered under the Exchange Act; |

| | the sections of the Exchange Act requiring insiders to file public reports of their share ownership and trading activities and liability for insiders who profit from trades made in a short period of time; |

| | the rules under the Exchange Act requiring the filing with the Securities and Exchange Commission (the SEC) of quarterly reports on Form 10-Q, containing unaudited financial statements and other specified information, and current reports on Form 8-K, upon the occurrence of specified significant events; and |

| | Regulation Fair Disclosure (Regulation FD), which regulates selective disclosures of material information by issuers. |

In addition, we will not be required to file annual reports and financial statements with the SEC as promptly as U.S. domestic issuers. Foreign private issuers are also exempt from certain more stringent executive compensation disclosure rules.

We may take advantage of these exemptions until such time as we are no longer a foreign private issuer. We are required to determine our status as a foreign private issuer on an annual basis at the end of our second fiscal quarter. We would cease to be a foreign private issuer at such time as more than 50% of the voting power of our issued and outstanding share capital is held by U.S. residents and any of the following three circumstances applies: (1) the majority of our executive officers or directors are U.S. citizens or residents; (2) more than 50% of our assets are located in the United States; or (3) our business is administered principally in the United States.

OUR PRINCIPAL SHAREHOLDER

Upon the consummation of this offering, Viking Capital Limited (our principal shareholder) will hold ordinary shares and special shares, which will represent approximately % of the voting power of our issued and outstanding share capital (or approximately % of the voting power of our issued and outstanding share capital if the underwriters exercise their option to purchase additional ordinary shares in full).

In connection with the issuance of Series C Preference Shares to our financial shareholders (as described below), we issued two warrants to our principal shareholder to purchase up to an aggregate of ordinary shares at an exercise purchase price of $0.01 per ordinary share. The number of warrants that vest is based on either the proceeds to our financial shareholders or the trading price of our ordinary shares starting 180 days after the date of this prospectus. The number of warrants that vest depends on the value per ordinary share, with 0% vesting at $ or lower price per ordinary share and 100% vesting at $ or higher price per ordinary share, and linear vesting between $ and $ per ordinary share. The vesting period for each warrant expires upon the later of February 8, 2026, or the sale, distribution or other transfer of 100% of the respective financial shareholders capital stock in us.

15

Table of Contents

CONFIDENTIAL TREATMENT REQUESTED BY VIKING HOLDINGS LTD

PURSUANT TO 17 CFR 200.83.

Our principal shareholder will have the ability to determine the outcome of all matters submitted to our shareholders for approval, including the election and removal of directors and any merger, amalgamation, consolidation or sale of all or substantially all of our assets. See Risk FactorsRisks Related to this Offering and Ownership of Our Ordinary SharesOur two-class structure has the effect of concentrating voting control with our principal shareholder, which could limit your ability to influence certain key matters affecting our business and affairs.

As a result of our principal shareholders ownership, we will also be a controlled company within the meaning of the rules of the NYSE. Under these rules, a company of which more than 50% of the voting power is held by an individual, group or another company is a controlled company and may elect not to comply with certain corporate governance requirements, including:

| | the requirement that a majority of the board of directors consist of independent directors as defined under the rules of the NYSE; |

| | the requirement that we have a compensation committee that is composed entirely of independent directors with a written charter addressing the committees purpose and responsibilities; |

| | the requirement that we have a nominating and corporate governance committee that is composed entirely of independent directors with a written charter addressing the committees purpose and responsibilities; and |

| | the requirement for an annual performance evaluation of the nominating and corporate governance and compensation committees. |